Top 10 Airlines Sites in the US (2025–2026): Passenger Traffic, Routes & Market Share

Business to Consumer

April, 25, 2026

Planning on traveling to some exotic location this year? Well, you are definitely not alone. The top airline companies in the US collectively carried more than 900 million people in 2024, according to the Bureau of Transportation Statistics (BTS), while also setting an all-time record for the highest monthly number of systemwide passengers at a remarkable 83.3 million for December 2024. But which are these airlines, and which flights are responsible for the massive growth in their business? Let us find out in this comprehensive guide, using data from OAG (Official Aviation Guide) — the global leader in aviation data services, as well as by BTS monthly enplanement reports filed directly by every commercial U.S. carrier.

1. American Airlines — America's Largest Carrier by Seat Capacity

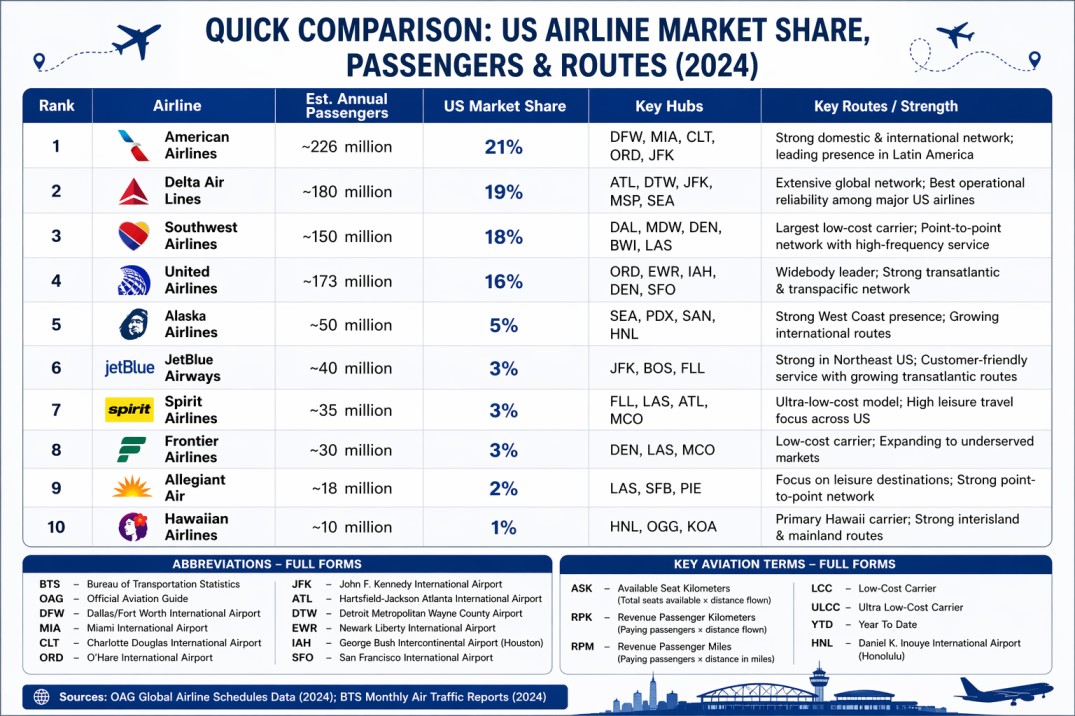

No airline in the United States or the world, for that matter, operates the largest seating capacity than American Airlines. This is evidenced by its performance according to OAG's full-year 2024 statistics — American scheduled 275.5 million seats across 2.2 million flights, both these metrics ranking first globally. The operator's market share stands at 21% (of total U.S. domestic capacity), which remains resilient despite challenges from Delta and Southwest.

Its hub network is specifically designed to serve each and every important traffic corridor: Dallas/Fort Worth (DFW) for the Sunbelt, Miami (MIA) for Latin America and the Caribbean, Charlotte Douglas (CLT) for the East Coast, and Chicago O'Hare (ORD) and Philadelphia (PHL) serving the Midwestern and Northeastern regions respectively. At Miami alone, American Airlines' share accounts for an approximate 57% of all passenger traffic — that is not a dominant presence, that is in fact a monopoly in everything but name.

However, the most important number here would be that American flew around 226 million passengers around the world in 2024, making it the leading airline in the world when measured on the basis of passenger numbers, according to Statista's ranking of the world's airlines by passenger volume. Its US aviation industry footprint is the benchmark everyone else measures against.

2. Delta Air Lines — The Reliability Champion of the US Aviation Industry

The story of Delta Air Lines is one of quiet dominance. It holds a domestic market share of 19%, operating a fleet tied at 1,006 aircraft (equal with American Airlines as per OAG 2024 data), and routinely features at the top in industry rankings for on-time performance. According to the OAG On-Time Performance Report of 2023 — the most recent comprehensive global ranking — Delta secured the top position among the largest global airline fleets in terms of operational reliability.

The secret weapon is Atlanta Hartsfield-Jackson Atlanta International Airport which stands as the world's single busiest airport. The connecting traffic volume of Delta's primary airport hub remains beyond reach for other airlines to match. The airline network achieves national coverage through its hub operations at Detroit (DTW), Minneapolis (MSP), New York (JFK), Salt Lake City (SLC), Boston (BOS), Los Angeles (LAX), and Seattle (SEA) which provide regular flight services. Delta carried approximately 180 million passengers in 2024 and posted revenues exceeding $60 billion, making it the most valuable U.S. airline by revenue, assets, and market capitalization — a fact confirmed by both OAG and publicly filed financial data.

3. Southwest Airlines — The Low-Cost Carrier That Redefined US Airline Market Share

Southwest Airlines is its own category. It does not operate hubs in the traditional sense like others do. Its point-to-point model connects destinations or cities directly — without forced layovers in Atlanta or Dallas. That's what makes its service appealing to leisure passengers who continue to use SwA services. As per OAG data for 2024, it holds 18 percent of the total seat capacity in the U.S., and an impressive 97.1 percent of all its scheduled flights are purely domestic, the highest concentration of any major U.S. carrier.

More than 100 American cities are on its network, anchored by Dallas Love Field (DAL), Chicago Midway (MDW), Denver (DEN), Baltimore/Washington (BWI), Las Vegas (LAS), and Phoenix (PHX). Its clearest differentiators include free checked bags and no change fees — in a market where Spirit and Frontier charge for everything from a window seat to a cup of water.

Southwest Airlines carried approximately 150 million passengers in 2024 and those passengers tend to be extraordinarily loyal. No airline in America has a more devoted domestic following among price-sensitive travelers.

4. United Airlines — Largest Airline Fleet of Widebodies, Biggest Global Reach

United Airlines has its own specific position at the top of the U.S. aviation market since it is the airline that is built for the global market of the United States. Though it holds 16% of the domestic market share, which places it in the fourth position, according to OAG data for 2024, United Airlines leads the world airlines in ASKs at 507.1 billion.

This is due to the fact that United Airlines uses the most widebody aircraft than any other U.S. carrier, thus providing nonstop flights to distant locations where narrowbody aircraft cannot reach. The seven domestic hubs in the United States include Chicago O'Hare (ORD), Newark (EWR), Houston (IAH), Denver (DEN), Washington Dulles (IAD), Los Angeles (LAX), and San Francisco (SFO) are spaced to maximize both domestic feed and international departure options.

Worldwide, United Airlines carried about 173.6 million passengers in 2024, and it has over 700 aircraft on order for delivery until 2033 — the most ambitious renewal plan to replace its fleet of any U.S. airline.

5. Alaska Airlines — West Coast Strength, Now Growing Globally

Alaska Airlines has been the quiet achiever of U.S. aviation for decades now. With only 5% market share within the country, Alaska is not among the Big Four of American airlines; however in its chosen segments, especially the Pacific Northwest and Western regions of the U.S., Alaska often looms larger than airlines of much bigger national presence.

2024 was transformational. With the acquisition of Hawaiian Airlines by Alaska, it instantly acquired trans-pacific routes, a fleet of Boeing 787s, and Hawaii inter-island connectivity. Together, the Alaska Airlines Group operates flights connecting more than 140 cities in the United States, Canada, Mexico, and the Pacific. Its primary bases include Seattle-Tacoma International Airport (SEA), Portland International Airport (PDX), and a growing San Diego (SAN) base. Trans-Atlantic flights to London and Rome have been scheduled for 2026; a definite milestone for what was previously known as a regional airline company just a decade ago.

6. JetBlue Airways — Premium Disruption in the US Airline Market

JetBlue does not fit neatly into any category. Despite having 3% domestic market share and being smaller than Alaska, JetBlue's premium Mint service with lie-flat seats at prices legacy carriers struggle to match has transformed the game for transcontinental routes. The two main routes where JetBlue competes against the Big Four include flights from JFK to LAX and Boston (BOS) to Los Angeles (LAX).

It has primary hubs in New York JFK, Boston Logan (BOS), and Fort Lauderdale (FLL). According to OAG 2024 data, the airline has 3.5 million seats per month while flying to more than 100 destinations in the United States, Caribbean, Latin America, and Europe. Given the strategic review of possible mergers, the future of JetBlue looks promising.

7. Spirit Airlines — Ultra-Low-Cost Volume Play

Spirit Airlines proves that airline market share USA rankings do not require a premium product. With domestic share of nearly 3% and approximately 3.7 million monthly seats per OAG November 2024 data, Spirit thrives by lowering the fare down to almost nothing and charging separately for everything else. Spirit Airlines has a network that is concentrated in the Southeast, East Coast, and Sunbelt — Fort Lauderdale (FLL), Las Vegas (LAS), Atlanta (ATL), and Orlando (MCO) are its important markets. The airline has undergone capacity cuts of around 28% year-on-year by mid-2025 per OAG — reflecting serious financial restructuring. However, Spirit continues operating a substantial domestic network in the meantime.

8. Frontier Airlines — Budget Routes Across American Heartland

Mirroring Spirit's ultra-low-cost model, Frontier Airlines is operating more heavily into the markets in the Midwest and Mountain West. According to OAG, Frontier makes up about 3% of total capacity in domestic terms, although it reduced about 12% of available seat miles from one year to another in 2025 in light of changing demand. The airline's network features connections for leisure purposes among smaller cities overlooked by the Big Four, and the low fares are appealing enough to prompt travelers to either drive or skip the trip entirely.

9. Allegiant Air — The Underserved Market Specialist

Allegiant Airlines has built one of the most unique and resilient business models in the U.S. airline industry. As opposed to the usual strategy of targeting crowded, high-demand routes that are mostly used by bigger companies, Allegiant Air offers connections between mid-sized cities and popular vacation destinations. Routes such as Provo to Orlando, Bozeman to Las Vegas, and Rockford to Phoenix may serve as examples. In these markets, Allegiant Air often operates without having any competitors.

This strategy works well. As per information from OAG, Allegiant had the best month-to-month capacity expansion among major U.S. airlines during November 2024, expanding by 22.1%. It is significant in the destinations where it operates even though it has a modest share of about 2% in the domestic aviation industry. Its key operational hubs are Las Vegas (LAS), Sanford/Orlando (SFB), and (St. Pete–Clearwater) PIE. In most of these small airports, Allegiant is more than a travel option; it is the only affordable non-stop option available to customers.

10. Hawaiian Airlines — Pacific Lifeline Under New Ownership

Hawaiian Airlines ranks at tenth position in the list. It is a small carrier compared to other airlines in the country, but it plays a very important role in maintaining connections between Hawaii and the rest of the world. The carrier recently went through a merger with Alaska Air Group in 2024, marking a whole new stage in the company’s development and integration.

Despite the fact that it represents only a minor part of the US market—1%, specifically—the airline is extremely significant for those who have to travel between Hawaii and the mainland. According to statistics from OAG, the airline operates 1.1 million seats monthly and mainly from Honolulu (HNL) and Maui (OGG). It connects these two islands with a lot of major US cities, including Los Angeles, San Francisco, Seattle, and New York.

U.S. Aviation Industry Trends (2025–2026): Market Share, Passenger Growth & What It Means for Travelers

The U.S. airline industry in 2025–26 is increasingly characterized by consolidation. The largest airlines in the USA — American Airlines, Delta Air Lines, Southwest Airlines, and United Airlines — control nearly 75% of total seat capacity, according to OAG's data of April 2026. This dominance continues to redefine — airline market share, pricing, and route competition within the United States. Apart from the Big Four, carriers like Alaska Airlines, JetBlue Airways, Spirit Airlines, Frontier Airlines, Allegiant Air, and Hawaiian Airlines constitute about 16 percent of total passenger movement in the United States, leaving little room for regional airlines.

Competition, however, is evolving. Ultra-low-cost carriers (ULCCs) such as Spirit, Frontier, and Allegiant are experiencing rising costs and stable demand levels that have led to slowing down of growth. Meanwhile, airlines like Alaska Airlines and JetBlue are focusing on global markets, expanding into transatlantic and transpacific routes to compete more directly with legacy carriers and reshape U.S. airline route networks. Passenger traffic is still healthy. The U.S. Bureau of Transportation Statistics (BTS) stated that total annual passenger traffic reached historic highs in 2024, attributed to strong domestic demand of 89.7 million passengers in June 2024 and steady international growth.

The disparity between major airlines and their competitors is widening. Each of the Big Four continues to improve their competitive advantage as follows:

- United Airlines is expanding globally by acquiring new aircraft fleets

- American Airlines fortifies its hub network

- Delta Airlines maintains its reputation for dependability and luxury services

- Southwest Airlines dominates domestic frequency

Conclusion: What This Means for Airline Passengers in the US

As far as travelers are concerned, the implications are straightforward but important. The major carriers account for almost all major routes; thus, in terms of how much choice travelers have, and what they will have to pay, competition between those companies becomes paramount.

If multiple major airlines operate a route, competition is likely to lower prices and raise the frequency of flights. On the other hand, routes with limited competition often reflect higher fares and fewer choices. This dynamic is crucial in determining how airfare is set in the contemporary U.S.

Ultimately, one should admit that the US air carrier market is characterized by a high degree of concentration and a high level of competition as well. Although the most successful carriers grow steadily and strengthen their dominance, evolving strategies from low-cost and mid-tier carriers ensure that competition remains alive — benefiting passengers through better connectivity, more choices, and, in many cases, more affordable travel.